The minimum income needed to qualify for a typical mortgage on a median-price home is higher than ever. The culprits: rising interest rates, high home prices and low inventory.

As of August, buyers needed an annual income of $114,627 to qualify for a 30-year fixed-rate mortgage on a median-priced U.S. home (costing $420,000), according to a study by Redfin. That’s about $40,000 more than the median national income and translates to a monthly house payment of $2,866, a record high.

To find the minimum income required to qualify in each of the 100 largest metro areas, the study assumed a 30-year fixed-rate mortgage at a 7.07 percent interest rate and a 20 percent down payment. Spending more than 30 percent of one’s income on housing was considered unaffordable in the study. Principal, interest, property taxes and insurance were included in the qualifying equation.

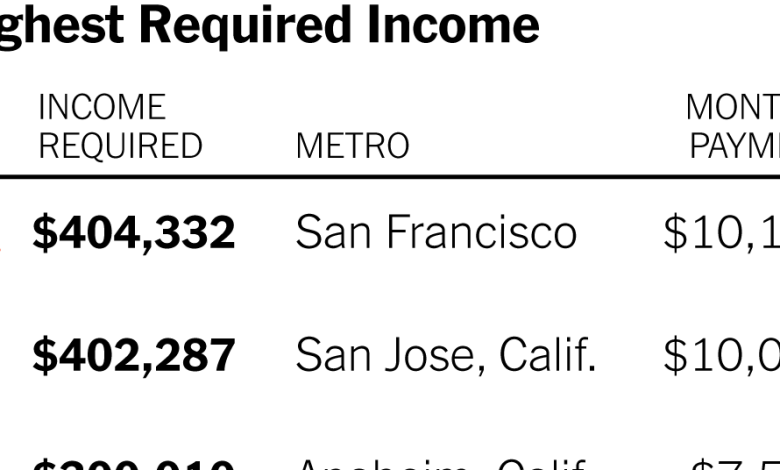

An income of at least $100,000 a year was needed to qualify for a mortgage in half the metros, and an income of $50,000 wouldn’t be enough in any of them. California metros took the top seven spots for required income. The greatest annual increases were in Newark and Miami, where the required income rose by 33 percent; the smallest was in Austin, Texas, about 8 percent. Midwest metros also saw comparatively low increases.

In hot spots of pandemic home demand — Austin, Texas; Boise, Idaho; Salt Lake City, Fort Worth, and Lakeland, Fla., among them — home prices fell during the year. But because of higher interest rates, the qualifying income for mortgage approval rose anyway.

This week’s chart shows the metros with the highest and lowest income requirements to qualify for a standard mortgage on a median-priced home, as well as the monthly payment that would result.

For weekly email updates on residential real estate news, sign up here.